I am currently teaching various courses on fiscal State aid. As always, we are having a miserable time dealing with the issue of material selectivity. Indeed, last week during class I was treated to the disconcerting spectacle of a frustrated participant, literally facedown on a table in the time old yoga pose, ‘downward student’.

The application of the selectivity component of Article 107(1) TFEU in direct tax cases has been proving troublesome for years now. This is an understatement. To be honest, the whole topic has started to remind me of the young Maria from the Sound of Music: elusive and slightly annoying.

Undaunted by the singing nuns, I want to take a moment to explore some of the vexing issues surrounding material selectivity in direct tax cases. (And just in case any students are reading this: answering the exam in blog-style bulletpoints is unlikely to have a happy ending.) In short, the type of (simplified) measure which has been giving us grief is as follows:

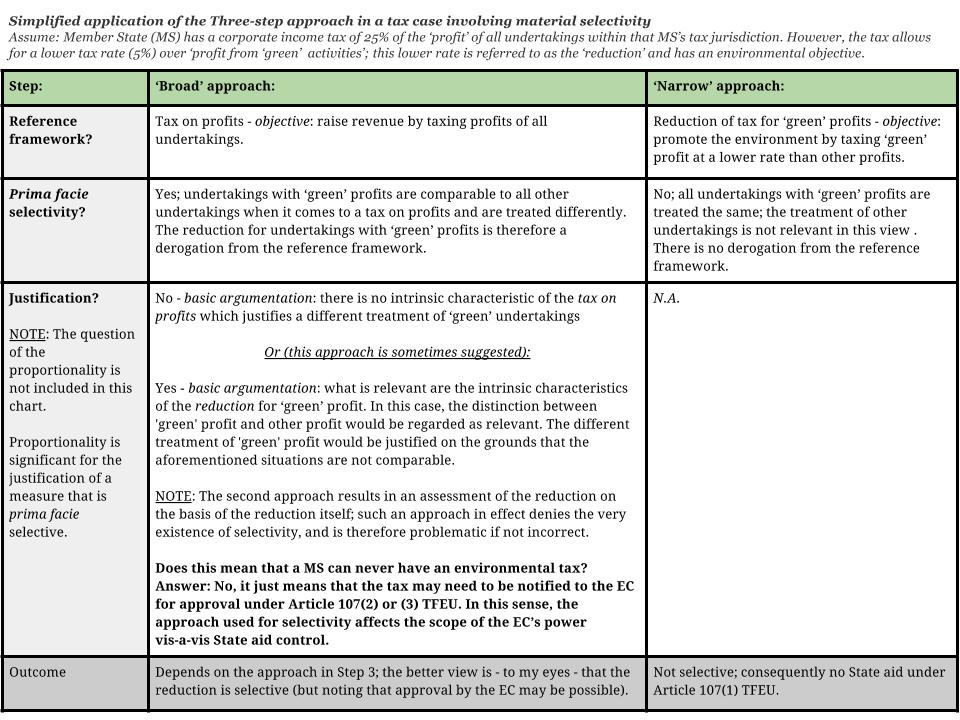

Member State (MS) has a corporate income tax of 25% of the ‘profit’ of all undertakings within that MS’s tax jurisdiction. However, the tax allows for a lower tax rate (5%) over ‘profit from ‘green’ activities’; this lower rate is referred to as the ‘reduction’ and has an environmental objective.

What many tax people find complicated, is how to assess the selectivity of this type of measure using the Three-step approach. I am not sure whether this is a ‘tax people-thing’ or whether the issues discussed below are also recognisable to a wider competition law audience.

Let’s start at the very beginning

Before we go any further, a word of caution. If the task is to analyse a State aid risk, we obviously need to start with Article 107(1) TFEU and the cumulative criteria specified in that provision. Do NOT jump straight to selectivity; if this measure fails one of the other tests of the State aid prohibition, it is game over! – without getting into the selectivity analysis at all. Assuming, however, that we do need to address selectivity, it makes sense to begin with a few critical assumptions and/or caveats. For example:

- Both the tax and the reduction have legitimate objectives (raise revenue via tax on all undertakings and environmental protection, respectively); we could also add that the case is above the de minimis threshold and – just to be on the safe side – that we’re not assessing any issues relating to the compatibility of aid or whether the aid is new or existing. Also, we could specify that the questions about regional or sectoral selectivity are not discussed either.

- Other elements relating to the (technical) design of the measures are also potentially relevant and should, therefore, be made explicit and – where possible – scoped-out of the analysis:

– No underkill or overkill in the personal scope of the tax on profits (all undertakings are taxed, irrespective of legal form or residency (so: both head offices and PEs are covered);

– No possibilities for abuse of either the tax or the reduction; proper monitoring and control by the MS; the rules are well enforced;

– No provision of selective advantage via tax rulings or ‘sweetheart deals’; the application of the tax has no discretionary elements;

– No scope for tax planning structures or for (cross-border) disparities; the possible impact of tax treaties is outside the scope of this analysis;

– Etc.

N.B. there are no extra points for: “it is assumed that the measure is not in any way selective”!

Three-step approach

Returning to the environmental reduction and its possible selectivity. Looking at the case-law of the CJEU, the decision-making practice and the 2016 Commission Notice on Article 107(1), we could address this issue using the ‘Three-step approach’:*

Step 1: Establish the framework of reference.

Step 2: Is there a derogation from the framework?

Step 3: If yes, can the derogation be justified?

A ‘derogation’ exists where situations which are comparable in light of the objective of the measure are nevertheless treated differently. In this sense, a comparability approach is pretty close to a derogation approach. A ‘justification’ is only possible on the basis of ‘intrinsic’ characteristics of the system of reference. Furthermore, the issue of proportionality is relevant (a different kettle of fish, to be boiled on some other occaision).

Basic questions re: the application of the Three-step approach in tax cases

When applying the Three-step approach, (at least) two questions tend to be problematic. Firstly, there can be uncertainty about the reference framework (more specifically: the (broad) tax on profits or the (narrow) environmental measure?) Note, however, that this is a legal question which requires careful examination; I won’t go into this in detail, but suffice to say there is no ‘one size fits all’ solution here.

Secondly, it is not always evident what can constitute a grounds for justification, although we do understand clearly that we should be looking at the nature and general scheme of the tax system. But what does this look like in practice? In the 2016 Notice, the EC gives a number of examples, including the prevention of double taxation or measures to combat abuse, but these do not always clarify matters. What is at any rate not possible, is to argue that a prima facie selective measure is justified because the measure was intended as prima facie selective. Furthermore, it is not possible to trump prima facie selectivity with a policy reason (along the lines of: “a prima facie selective measure can be justified because it is geared towards saving whales.”) (This is less draconian than it sounds, as a State aid for the preservation of the marine environment (in this case) can conceivably be approved by the EC. The discussion about selectivity is very much about the scope of the EC’s regulatory powers and the fundamental limits of the fiscal sovereignty of the MS.)

The above is summarised in the following schematic overview. (printable version)

Comments:

- Not a mathematical exercise

The unofficial terminology of a ‘broad’ approach vs. a ‘narrow’ approach will be recognisable to many tax people, but is actually misleading in that it suggests there could be two equally valid approaches to selectivity in any given case, i.e. that the choice for a particular reference framework is entirely free/random, when in reality this aspect of the Three-step analysis must be based on a precise legal analysis. Furthermore, the application of a contrario logic (“under the narrow approach a measure is not problematic, therefore we can conclude the measure is not at all selective”) is not without problems, as material selectivity can arise from different places. Bottomline: like transfer pricing, the Three-step approach is “more an art than a science”. Sorry.

- Fiscal sovereignty

One of the central themes of EU law is the constant need to balance the issue of tax sovereignty of MS with the needs of the internal market. Like the fundamental freedoms, the State aid rules are a form of negative harmonisation, meaning that this balancing act is especially acute. When analysing any rules, the departure point must be the sovereignty of the MS, i.e. a MS can design its tax system as it damn well sees fit, within the constraints of the EU rules of course.

- Legitimate objective

In my view, fiscal sovereignty entails that any objective – with the exception of the objective to provide State aid – should be regarded as legitimate in the context of the State aid analysis. Whilst it is true that objectives such as environmental protection, R&D&I, etc. are Union objectives, this is not the reason why they are legitimate. Their legitimacy follows directly from the sovereignty of the MS. The alternative approach would result in a greater degree of harmonisation in the field of fiscal State aid than is presently the case.

- Not yet crystallised

The application of the Three-step approach in tax matters is currently subject to debate: should there be a ‘broad’ approach? Or is a ‘narrow’ approach better? Also, there are questions regarding the relationship between a ‘comparability’ approach and a ‘derogation’ approach. Without wanting to suggest that the application of the State aid rules in fiscalibus is beyond all human comprehension (that would be too alarmist), I am not comfortable presenting ‘the’ definitive step-by-step plan for material fiscal selectivity. And let’s not forget: various crucial cases are still before the CJEU, e.g. the appeal in Heitkamp Bauholding (T-287/11) and all of the recent transfer pricing cases (Apple, Starbucks, etc.)

- Never be clever

The next point concerns the so-called ‘effects doctrine’. It is settled case-law that State aid must be assessed according to its effects and not is specific legal form. State aid is focussed on the impact of measures, not their technical appearance. Consequently, we need to be critical of any measure of national law which seeks to avoid the classification as State aid via ‘clever’ technical approaches. The Gibraltar case (C-106/09 P and 107/09 P) is a case in point: here, the CJ did not accept that the State aid rules could effectively be circumvented via the use of three (seemingly independent) taxes as opposed to one exemption from tax. One consequence of the effects doctrine is therefore that when applying the analysis for material selectivity, we need to maintain an open mind: are we sure that we are not looking at a ‘clever’ technical approach aimed at obscuring the classification as State aid?

- Gray area

When it comes to material fiscal selectivity, “What is the right answer?” is simply not the right question. As the law currently stands, multiple perspectives on the selectivity issue exist with as many solutions and outcomes. Understanding the differences between these approaches and their strengths and weaknesses is – until further notice and in my opinion – what matters most.

***

* I am not convinced that this traditional approach to analysing selectivity in tax measure is the most sensible one (in 2013, I published an article on this with professor Frank Engelen (University Leiden), arguing for an alternative ‘stepplan’). See also here for a good article on different ‘types’ of material selectivity.

Photo of clouds by edward stojakovic via Flickr.com (under Creative Commons licence; checked d.d. 5 March 2017).

Please note: I have made a few minor corrections since the first publication on 5 March 2017.

I hope the yoga-master student was not me. Very insightful article nevertheless.

Thanks!